Thin capitalisation in the UAE: A forward-looking perspective

Deepali Aggarwal

by Deepali Aggarwal

Thin capitalisation rules can seem confusing, especially when navigating new corporate tax laws in the United Arab Emirates (UAE). In this article, we simplify the regulations and show you how to adapt without stress.

Thin capitalisation refers to a situation where a company is financed through a relatively high level of debt compared to equity.

Why the need for a thin capitalisation norm?

Multinational enterprises (MNEs) often structure their financing arrangements to maximise these benefits by establishing a tax-efficient mixture of debt and equity in borrowing countries, influencing the tax treatment of the lender which receives the interest. As a result, nearly 70% of multinational corporations have had their tax strategies challenged due to excessive debt financing.

Example:

Two companies – X (lender) and Y (borrower) – belonging to the same MNE group may be structured in a way that allows the interest to be received in X’s jurisdiction that either does not tax the interest income, or which subjects such interest to a low tax rate. Company Y, operating in high tax jurisdiction, claims a deduction on interest paid to company X, resulting in base erosion.

The UAE aligns more with the Organization for Economic Co-operation and Development’s (OECD) approach of base erosion and profit shifting (BEPS) Action 4 principles. It aims to limit base erosion through the use of interest expense to achieve excessive interest deductions or to finance the production of exempt or deferred income.

Issue identified by the OECD

Multinational groups may achieve favourable tax results by adjusting the amount of debt in a group entity.

BEPS risks in this area may arise in three basic scenarios:

Groups placing higher levels of third-party debt in high-tax countries.

Groups using intragroup loans to generate interest deductions in excess of the group’s actual third-party interest expense.

Groups using third party or intragroup financing to fund the generation of tax-exempt income.

To discourage excessive debt financing, restrictions on deduction of interest expense, the OECD aims to limit base erosion with the help of BEPS Action Plan 4.

This is likely to influence the following entities:

Multinational enterprises (MNEs) with significant related-party debt transactions;

Free zone entities that engage in related-party transactions involving debt;

Large local businesses with intercompany loans or high levels of debt financing;

Entities with high debt-to-equity ratios, indicating reliance on debt;

Related entities with cross-border financing arrangements; and

Businesses with substantial interest deductions from intercompany loans.

UAE’s approach

UAE tax law follows the fixed ratio approach, out of three methods recommended by BEPS Action Plan 4.

Article 30 of the Decree Law (UAE Corporate Tax Law: Ministerial Decision No. 126 of 2023 on the General Interest Deduction Limitation Rule for the Purposes of Federal Decree-Law No. 47 of 2022 on the Taxation of Corporations and Businesses) provides the General Interest Deduction Limitation Rule:

Net interest expenditure* is deductible up to an amount greater than of 30% of earnings before interest, taxes, depreciation, and amortization (EBITDA) – excluding exempt income; or AED 12 million.

The Un-utilised interest amount from a tax period can be carried forward for the next 10 tax periods.**

Interest expenditure shall be deductible in the tax period in which it is incurred.

Interest expenditure disallowed under any other provision of this decree law shall be excluded from the calculation of net interest expenditure.

The general interest deduction limitation is not applicable:

Where net interest expenditure does not exceed the “safe harbour” limit (to be specified by the Minister of Finance;

To banks, insurance providers, or any specified person (who may be specified by the Minister in the future);

To a natural person undertaking business or business activity in the UAE;

For entities consolidating their financials because of applicable accounting standards, limit to be specified.

* Net Interest Expenditure:

Particulars

Amount (AED Millions)

Interest expenditure for the tax period

60

Add: Net interest expenditure brought forward

16

Less: Taxable interest income for the tax period

(40)

Less: Interest expenditure disallowed under any other provision of CT Law

(5)

Net interest expenditure

31

**Note - Losses/net interest expenditure of period covered by Small Business Relief (turnover up to AED 3 million), cannot be carried forward.

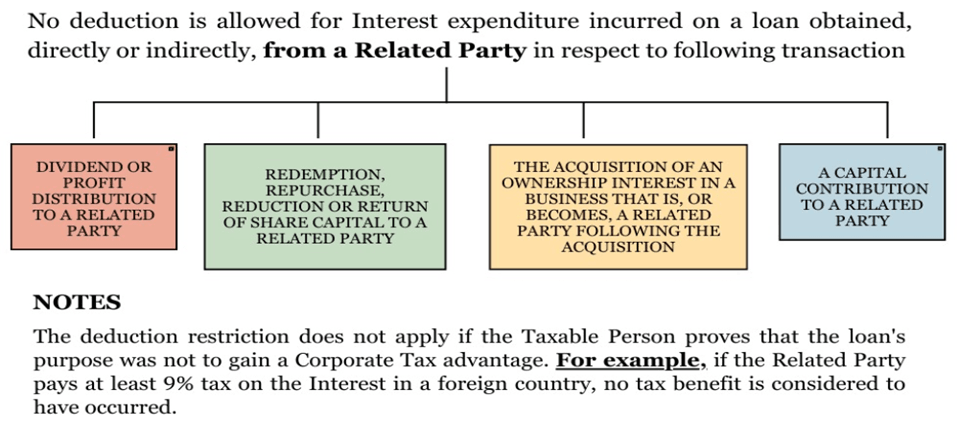

Furthermore, Article 31 of the Decree Law provides a Specific Interest Deduction Limitation Rule – Related Party Loan.

GGI member firm Ashwani & Associates, Chartered AccountantsLudhiana, IndiaT: +91 98554 00428

Advisory, Auditing & Accounting, Corporate Finance, Tax

Ashwani & Associates is an audit, tax and consulting firm in India with three offices. Their clients range from emerging entities to large corporations with billions of dollars of revenue. They include privately-held businesses, not-for-profit organisations, and publicly traded companies. Ashwani & Associates supports a local, national, and international client base.

Deepali Aggarwal is a tax Associate at Ashwani & Associates. She has over 3 years of experience in auditing, advisory, taxation, and consulting.

Contact Deepali